Principles for declaring triangular transactions

Source: Estonian Tax and Customs Board, Taxes and payment → Value added tax → Taxation of goods

All parties involved in the transaction must be VAT-registered in different Member States.

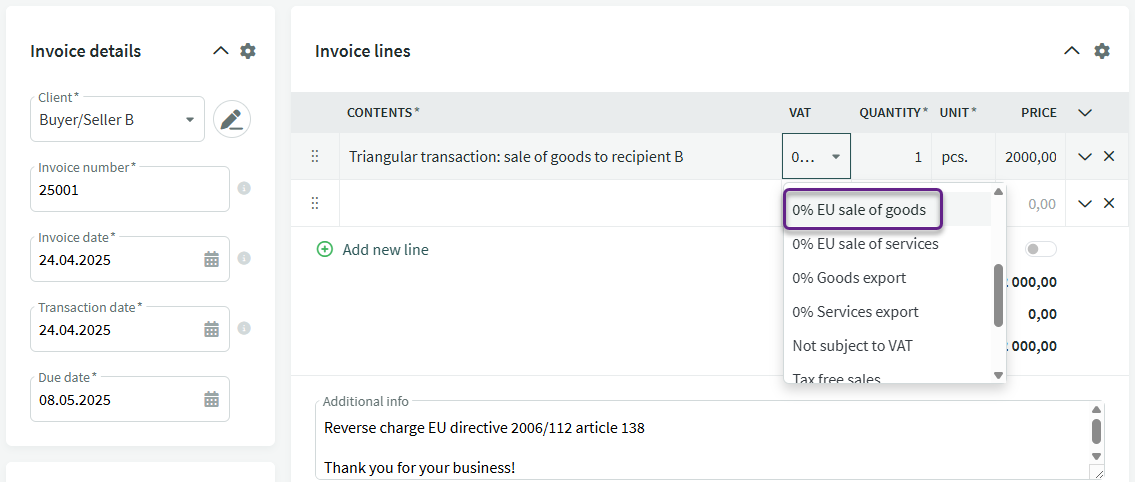

The first seller A declares as follows:

- the sale to B must be declared as intra-Community supply of goods in a VAT statement,

- the value of the sale must be declared in the report on intra-Community supply as regular supply (not triangular).

The sales invoice is a regular intra-Community supply of goods, with the VAT type set to 0% EU sale of goods.

The sale is reported on lines 3, 3.1, and 3.1.1 of the VAT return, and additionally in the VD report as a sale of goods (column 3).

The second seller B declares as follows:

- B declares the goods sold to C in the intra-Community supply report, in the “Triangular transaction” field;

- if B has other intra-Community sales of goods to C, these are declared separately in the intra-Community sales report, apart from the triangular transaction sales.

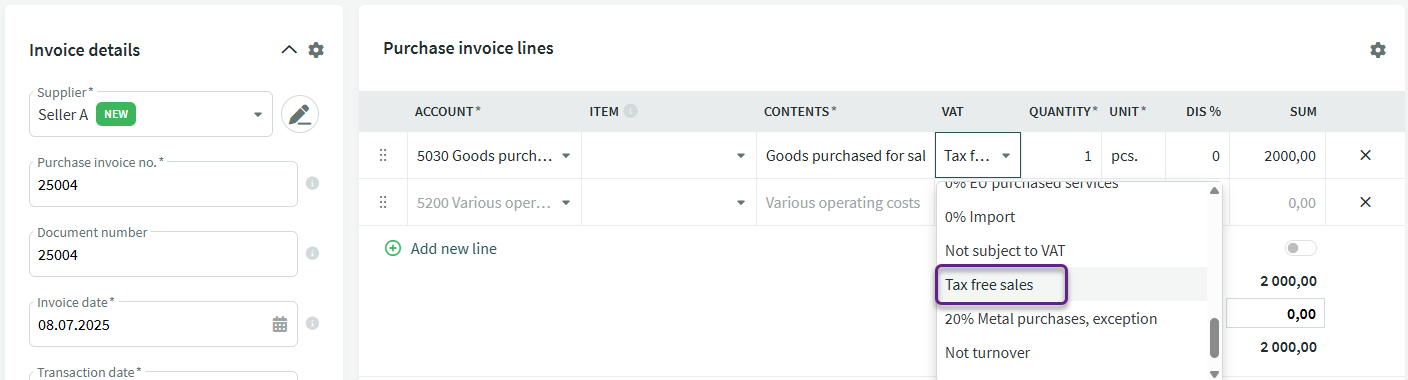

However, B does not declare the goods purchased from A as an intra-Community acquisition, nor the sale to C as an intra-Community supply of goods in the VAT return.

Entering the purchase invoice received from seller A into the accounting records of buyer/reseller B. The purchased goods are recorded as expenses and are not reported in the VAT return under the reverse charge rule. Therefore, we recommend using cost account 5030 Goods purchased for sale and setting the VAT type to “Tax free sales.”

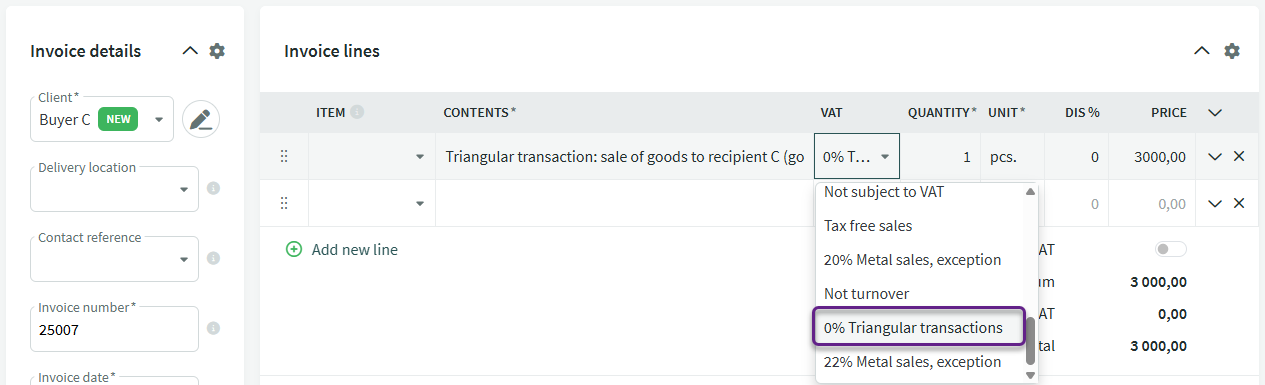

Issuing the sales invoice by buyer/reseller B to buyer C. The sale should be reported only in the VD report under the “Triangular transactions” column (column 4). The invoice should use the VAT type “0% Triangular transactions”.

The second buyer C declares as follows:

- the purchase from B is reported in the VAT return in field 1 or 2, depending on the applicable tax rate;

- VAT on the acquisition must be calculated in line 4 of the VAT return, and

- if goods for which the right to deduct input VAT has been acquired, the amount of VAT calculated must also be shown as deductible input VAT in line 5 of the VAT return, and

- in addition, the acquisition must be reported in the informational line 7 of the VAT return.

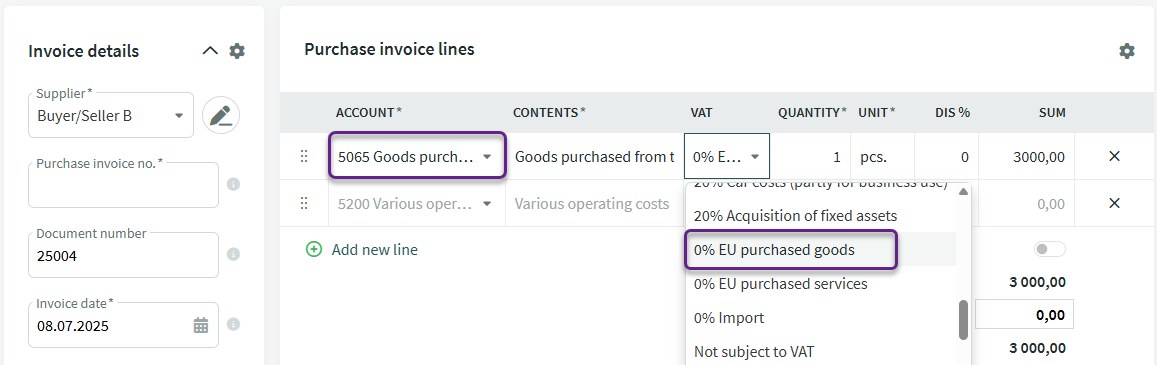

The goods recipient (the second buyer) records the purchase invoice as an intra-Community acquisition of goods, which is reported in lines 1 and 7 of the VAT return under the reverse charge mechanism

It is recommended to use financial account 5065 “Goods purchased from the EU (triangular transactions)” and assign it to line 7 in the VAT report settings, with the VAT type set to 0% EU purchased goods.

If you have any additional questions, please write to us at support@simplbooks.ee

Leave A Comment?