A prepayment invoice has been received from the supplier and paid immediately. The goods or services will be received in the following month. Both parties are VAT-registered, and the input VAT is claimed back in the month the prepayment is made. If the net amount is 1000 euros or more, it must be declared in Annex B of the VAT statement (KMD INF B).

Numbers used in the example (VAT 24%):

Total value of goods: 3500 euros + value added tax 840 euros = 4340 euros

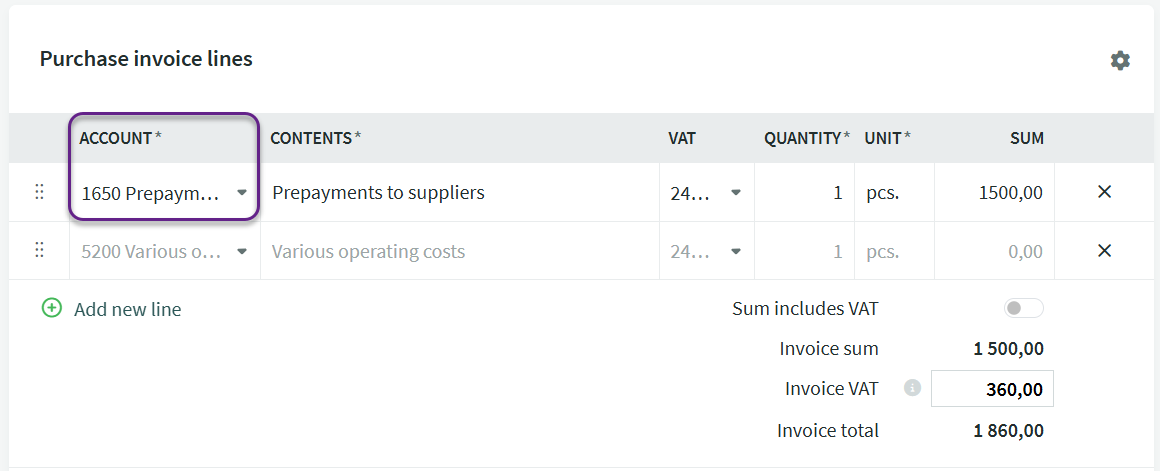

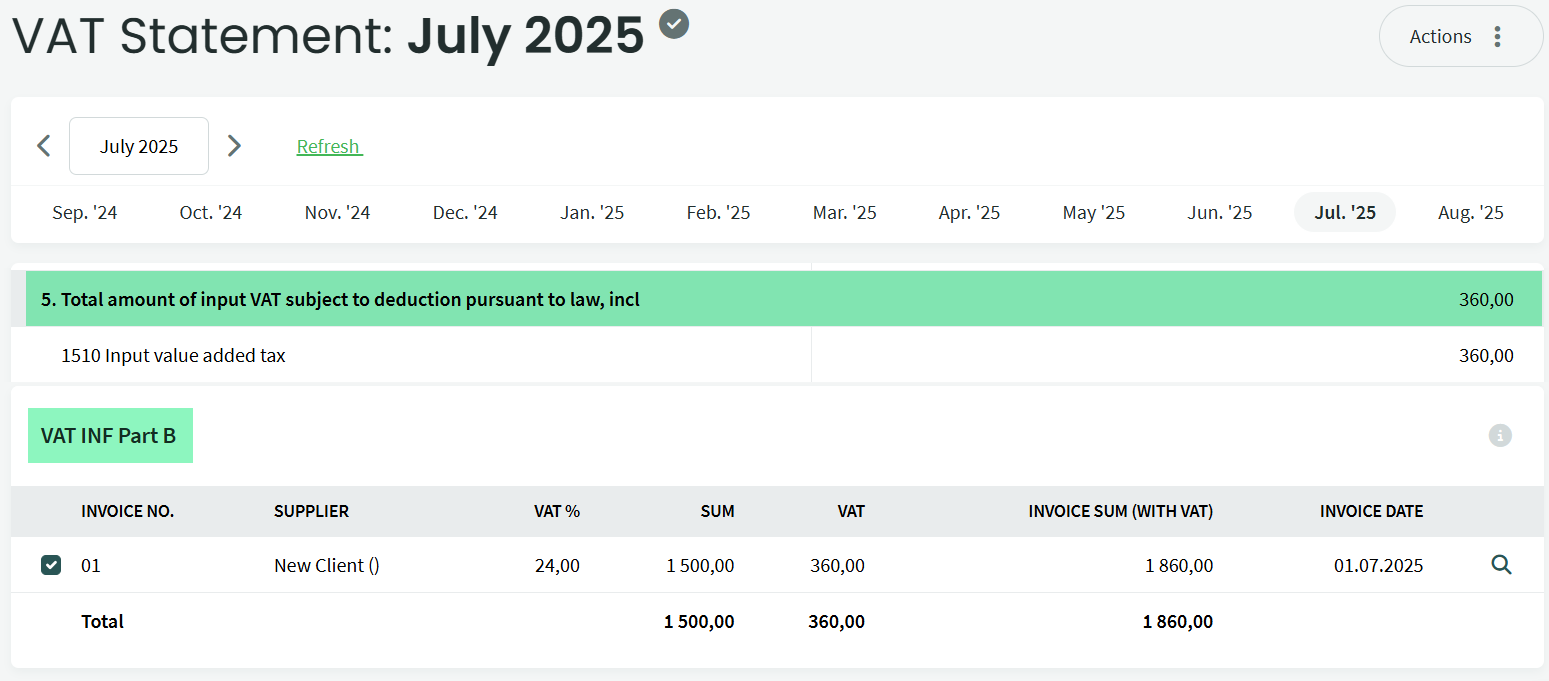

Prepayment: 1500 euros + value added tax 360 euros= 1860 euros (invoice received and paid in July)

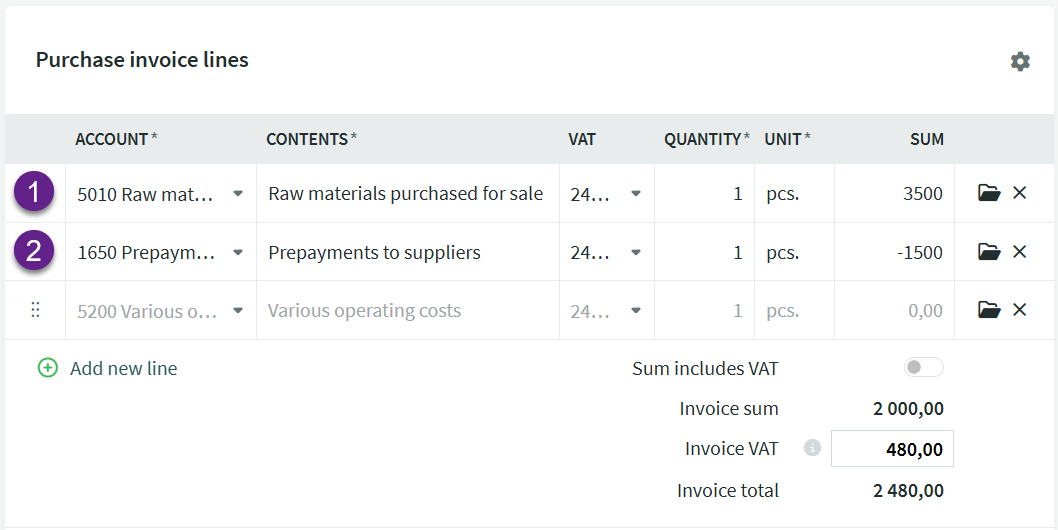

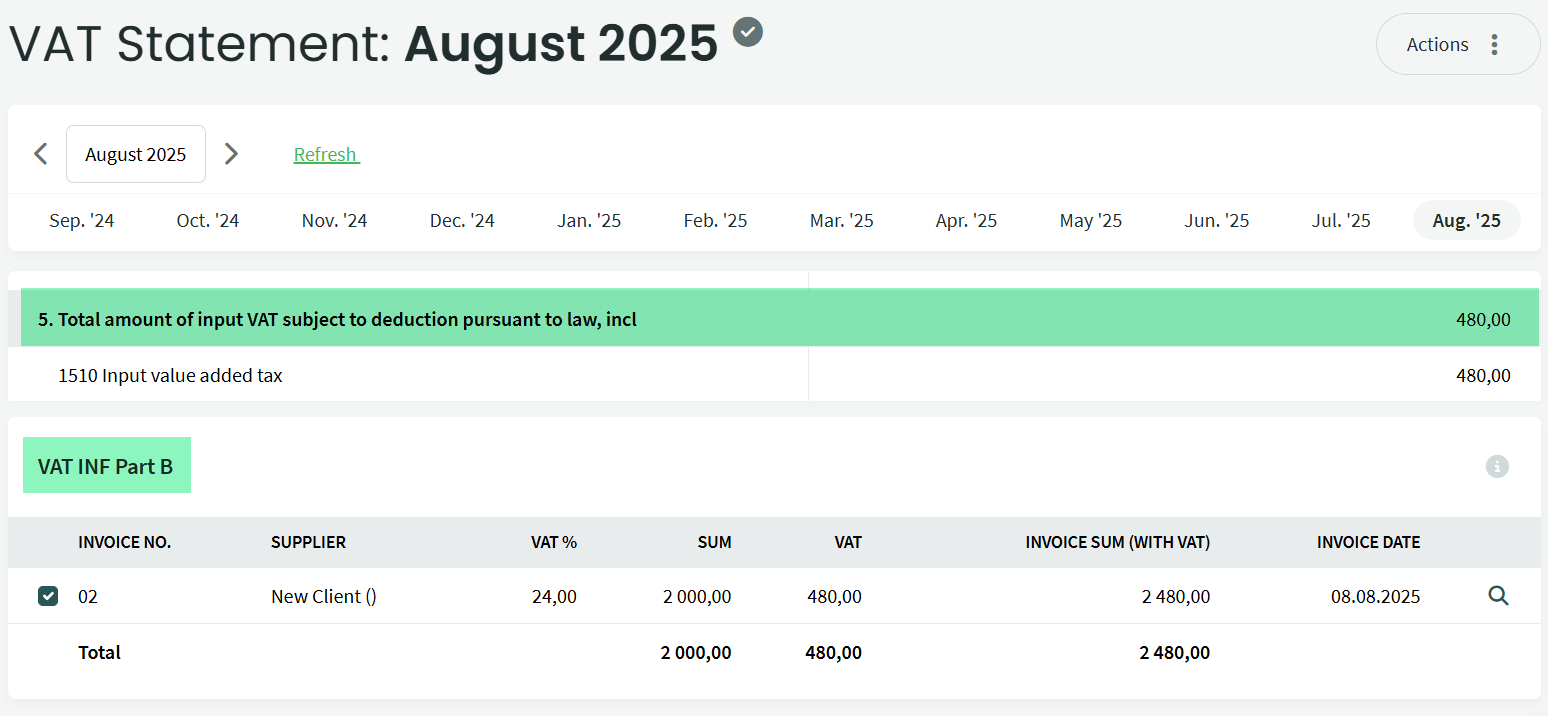

Final invoice: 3500 euros (on the expense line), prepayment 1500 euros (as a negative). The invoice shows value added tax in the amount of 480 euros (goods and invoice received in August).

Enter the prepayment invoice received from the supplier under Operations -> Purchase invoices.

It is important to note that when selecting the account on the line, you should use either account 1650 Prepayments to suppliers or account 1530 Prepaid expenses for future periods.

Link the invoice to the payment as usual.

Upon receipt of the goods or services, enter the final purchase invoice so that on the first line you add the expense account and the full expense amount (1) and on the second line you add the prepayment account used when entering the prepayment invoice (2). The VAT type must be the same on both lines to ensure correct data recording.

Entering it this way results in the correct amount on the expense account, the prepayment account balance being cleared, and the correct VAT amount appearing in the VAT statement.

The result must be that the total input VAT reclaimed from the two purchase invoices (prepayment invoice + final invoice) equals the total VAT calculated from the total amount, i.e., 360+480=840 euros.

If you have any additional questions, please write to us at support@simplbooks.ee

Leave A Comment?