Receivables from customers need to be reviewed at each reporting date. All available information must be taken into account.

For example:

- possible bankruptcy or financial difficulties of the debtor

- late payments or changes in payment behavior

- a drop in the debtor’s credit rating

You can check receivables one by one or all together. Bigger amounts should be checked individually. Smaller ones can be reviewed as a group. Historical data on past due receivables can be used to estimate potential losses when assessing receivables collectively.

The first step is to assess which receivables are unlikely to be collected and to recognise them as an expense. A receivable becomes a bad debt when there is reliable information indicating that the buyer is insolvent, at which point the receivable is written off from the balance sheet.

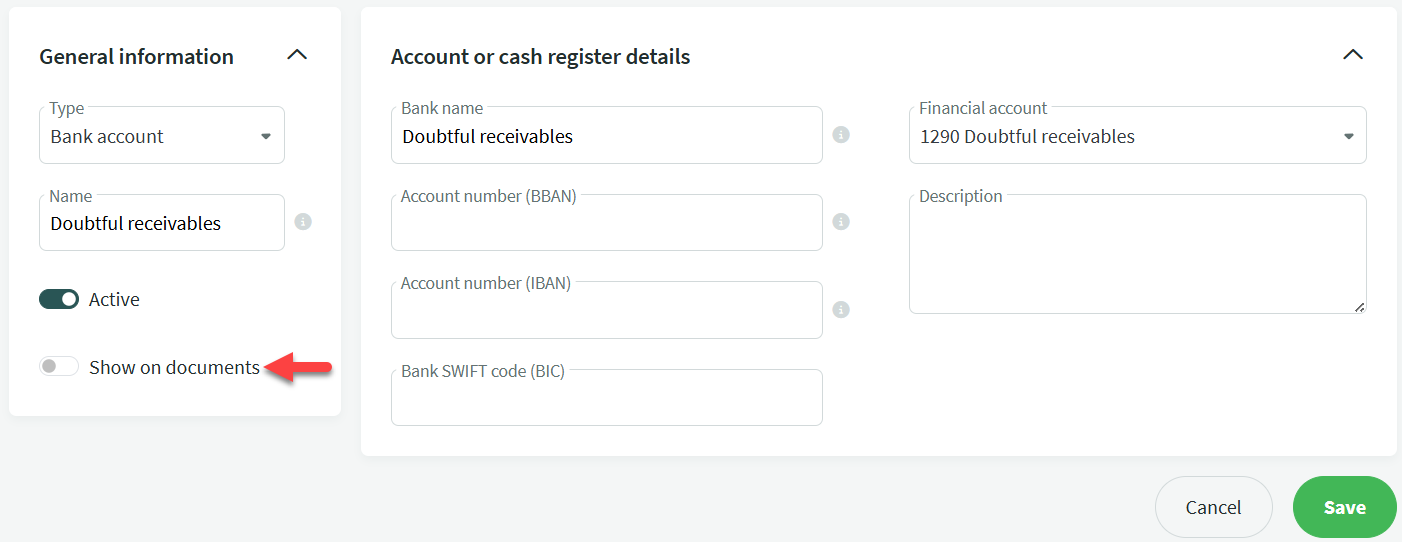

To write off a receivable from the balance sheet and ledger, it is necessary to create a new account under “Accounts and cash” (if it hasn’t been created previously).

Settings -> Accounts and cash ->

A transaction is created for the receipt:

Debit: 1290 Doubtful receivables

Credit: 1210 Trade receivables

The data should now be correct. It is still useful to check the sales ledger (Reports -> Sales ledger) and the balance sheet balances (this check should also be done before writing off receivables).

Since 1 January 2022, the VAT Act includes new rules that allow taxable persons to reduce their VAT liability if certain conditions are met and the receivable has become a bad debt.

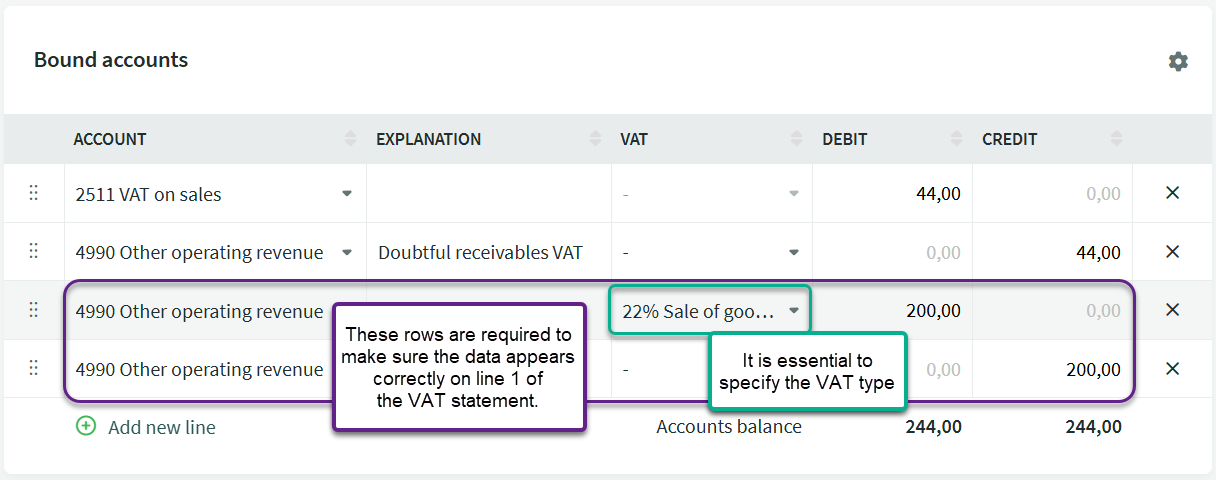

To reclaim VAT, a financial transaction must be recorded and the VAT statement settings need to be adjusted to ensure the data is reported correctly.

In the transaction, record the VAT amount on account 2511 VAT on sales in the debit and 4990 Other operating revenue in the credit.

On the next two lines, also use account 4990 Other operating revenue and enter the amount of the written-off invoice excluding VAT. On the line where the amount is recorded in the debit, make sure to also select the sales VAT type (in this example, 22% Goods sales, Estonia). This is necessary for the debit side of the account to be reflected in line 1 of the VAT statement.

Update the VAT report settings and add the account 4990d to the account rules on line 1 under the relevant VAT type.

If you have any additional questions, please write to us at support@simplbooks.ee

Leave A Comment?