When an operating lease agreement is concluded, an initial payment invoice is usually issued. The amount is first recognized in the balance sheet as a prepaid expense and recorded as an expense over the lease term.

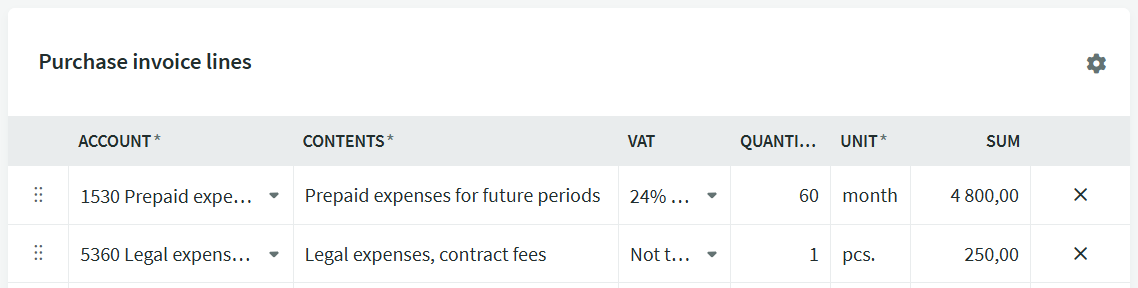

An example with a lease period of 5 years (60 months) has been used. The leased asset is a van, so the VAT type applied is 24% Estonia. For a passenger car, the VAT type should be selected based on its usage (100% or partial).

The first line is suitable for account 1530 Prepaid expenses for future periods. In the quantity field, you can enter the rental period length in months and in the amount field, enter the down payment amount excluding VAT. When saving the invoice, you will also see the monthly amount.

For the contract fee line, use account 5360 Legal expenses, contract fees.

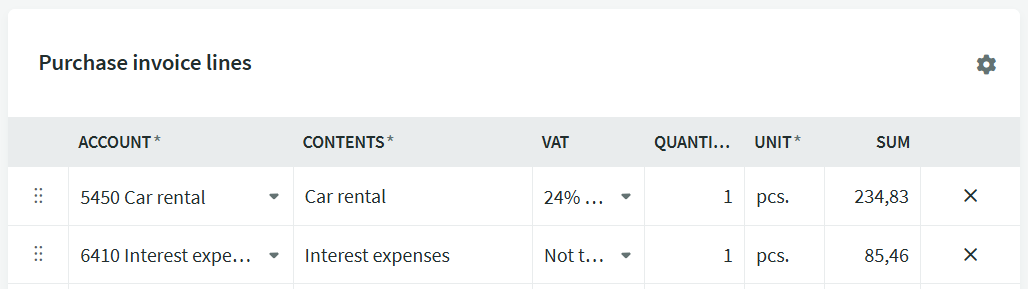

The monthly invoices specify the principal payment and interest. The suitable expense account for the principal payment is 5450 Car rental and for interest expenses, it is 6410 Interest expenses. If necessary, you can add more accounts, but make sure that they are reflected in the correct lines of the profit and loss statement.

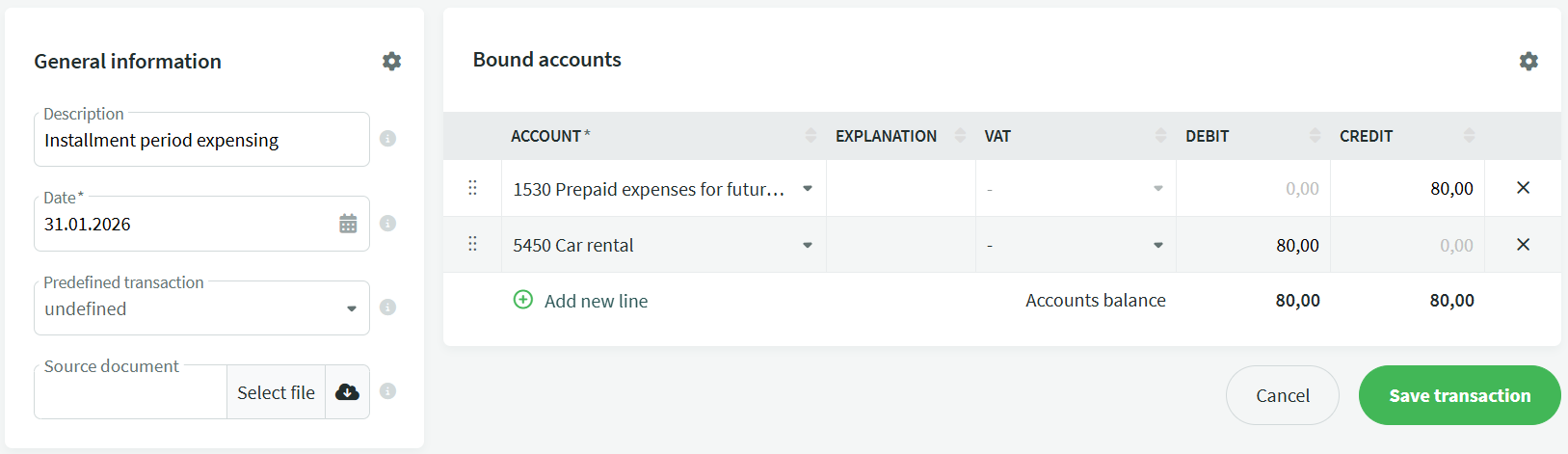

The expense transaction for the first installment can be made either monthly or annually. It is recommended to make monthly expense entries, as this ensures that the profit and loss statement always contains up-to-date information.

Accounting -> Transactions -> New transaction

If desired, you can add a where you specify the necessary accounts making the expense transaction entry process faster.

If desired, you can add a where you specify the necessary accounts making the expense transaction entry process faster.

You can also create transactions with future dates, so for example you can record the entire year’s expense transactions at the beginning of the year (assuming the company doesn’t plan to dispose of assets during the year). When copying the transaction, you’ll only need to change the transaction date

Useful reading:

ASBG 9 Accounting for leases

ASBG 5 Property, plant and equipment and intangible assets

All translations of the Accounting Standards Board guidelines can be found on the Ministry of Finance website.

If you have any additional questions, please write to us at support@simplbooks.ee

Leave A Comment?