Assets acquired under capital lease terms are usually intended for long-term use by the company and are recorded as fixed assets.

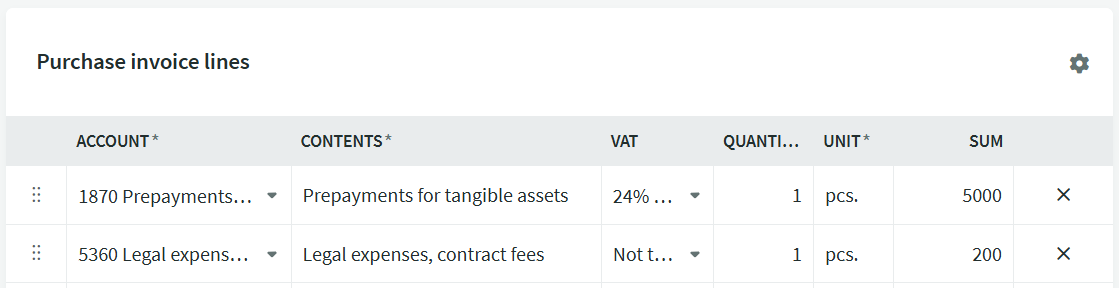

Enter the advance invoice as a purchase invoice, posting the first installment amount to account 1870 Prepayments for tangible fixed assets (VAT type 24% Acquisition of fixed assets). The contract fee should be posted to expense account 5360 Legal expenses, contract fees.

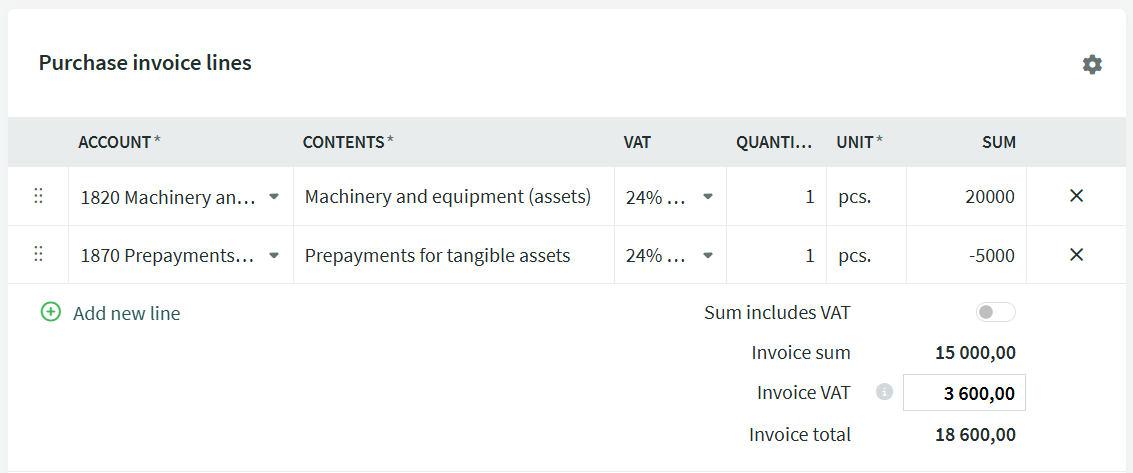

On the second line, choose account 1870 Prepayments for tangible fixed assets (for VAT type, select 24% Acquisition of fixed assets) and enter the amount of the first payment as a negative value.

When saving the invoice, enable the creation of the fixed asset card only for the first line, which reflects the total amount of the fixed asset. Remove the selection of account 1870 for this line. Afterward, review the depreciation accounts, depreciation rate, and make any necessary adjustments on the fixed asset card.

If there is no separate purchase invoice, the supporting document is the capital lease agreement along with the payment schedule. For more information on fixed assets, refer to the guide Recording of fixed assets.

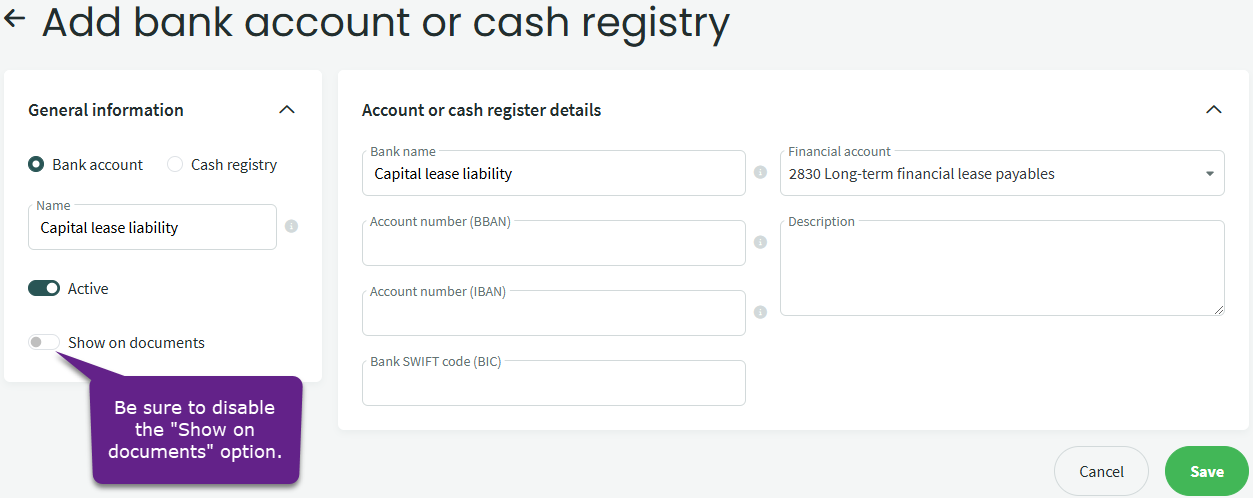

To record a long-term capital lease obligation, you need to create a new account by going to Settings -> Accounts and cash -> New Account/Cash register. Name it something like “Capital lease liability” and set the financial account to 2830 Long-term financial lease payables.

Make sure to set the “Show on Documents” option as inactive.

Mark the invoice as paid using the created account “Capital lease liability“.

When this payment method is used, a financial entry will be generated, reducing the account 2310 trade creditors and recording the long-term capital lease obligations in the balance sheet.

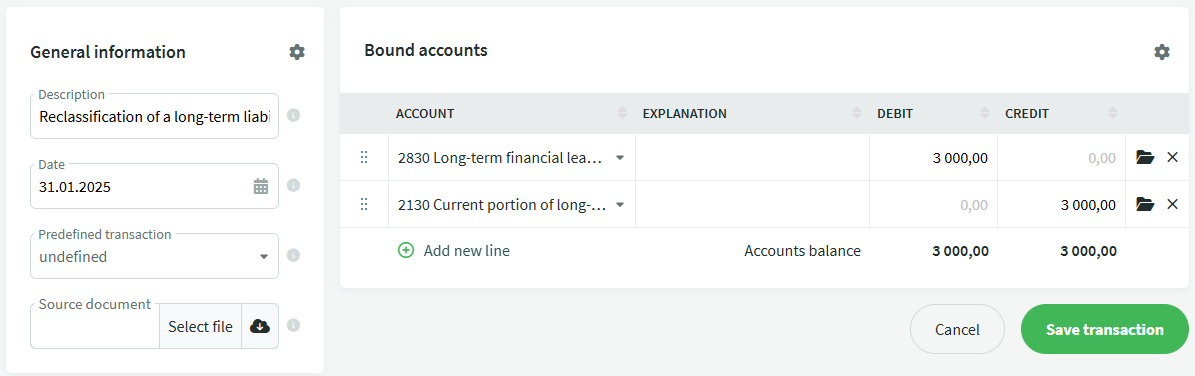

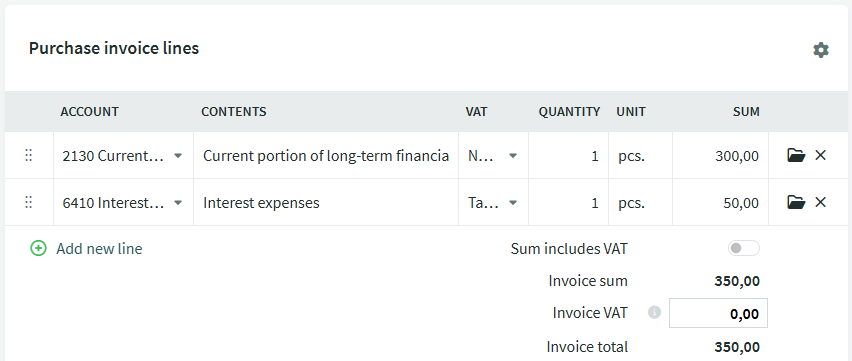

To allocate the short-term portion of the capital lease liability, a financial entry must be made. The first entry should be made with the date of the capital lease agreement and the amount to be repaid in the current fiscal year should be recorded as the short-term portion.

At the end of each fiscal year, an entry must be made to transfer the long-term portion to the short-term portion until the long-term liability is fully settled.

Useful reading:

ASBG 9 Accounting for leases

ASBG 5 Property, plant and equipment and intangible assets

All translations of the Accounting Standards Board guidelines can be found on the Ministry of Finance website.

If you have any additional questions, please write to us at support@simplbooks.ee

Leave A Comment?