Also, make sure to mark this in the Company profile.

Output VAT is recorded on sales invoices, which represents the tax liability to the Estonian Tax and Customs Board.

Input VAT is recorded on purchase invoices and can be reclaimed from the Estonian Tax and Customs Board if the expense is business-related.

On the VAT statement, the calculation is as follows: output VAT – input VAT = VAT payable (or VAT prepayment).

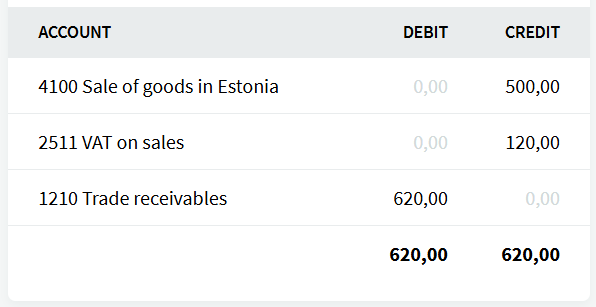

Example of a sales invoice transaction (sale of goods):

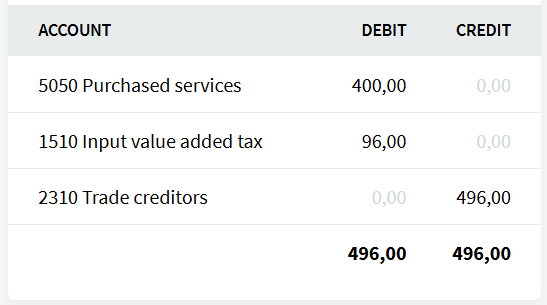

Example of a purchase invoice transaction (purchase of a service from an Estonian VAT-registered supplier):

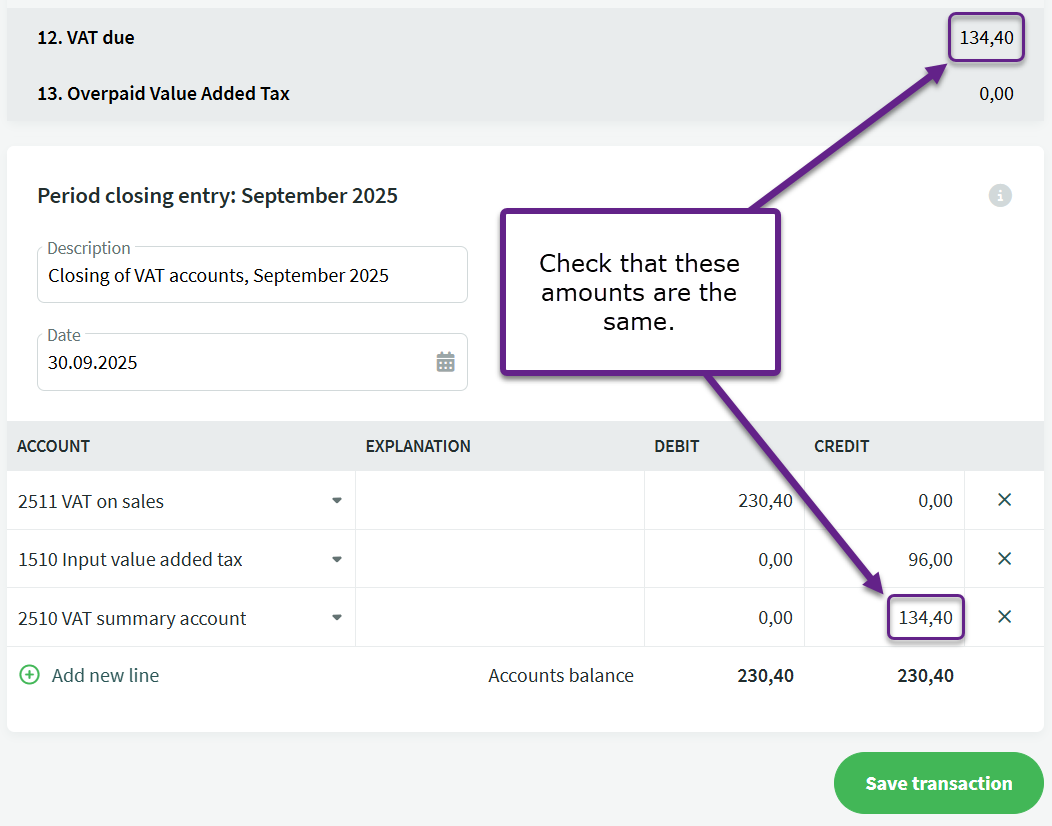

The closing entry can be found under the VAT statement for the respective month. This entry clears the output VAT and input VAT accounts, and records the VAT amount payable or overpaid for the period on the VAT summary account.

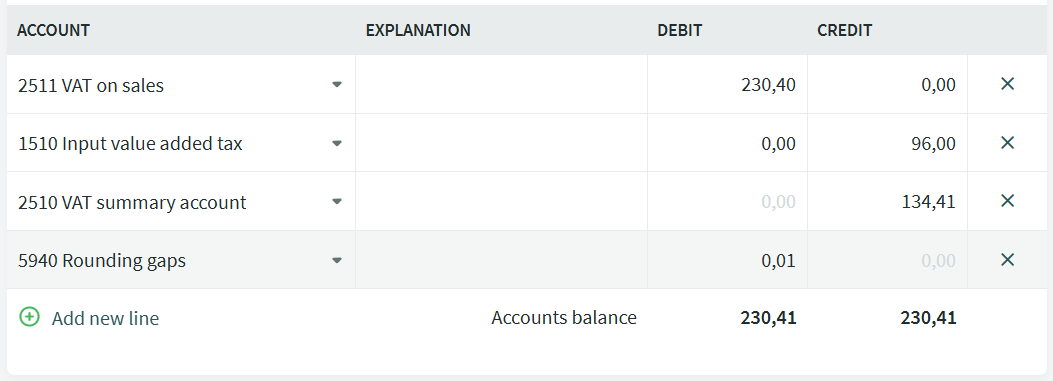

With the current VAT rate (24%), the difference may occasionally be up to around 5 euros. The exact amount depends on the number and size of invoices. To verify this, you can export the VAT report (Reports -> VAT report) and use formulas in Excel to check the calculated output VAT totals.

Important The period closing transaction must not be created manually, as this would cause the statement to display incorrect results when verifying the data later.

● If you have made a bank transfer to the Tax Authority’s account after submitting the declaration, you need to enter a financial transaction in the system for this payment. This can be done under Accounting -> Transactions by clicking the New transaction button in the upper right corner of the transaction list, or the transaction can be recorded automatically during the bank import process.

● Additional information on VAT-related transactions can also be found in the guide Frequently used accounting transactions, section 6.

If you have any additional questions, please write to us at support@simplbooks.ee

Leave A Comment?