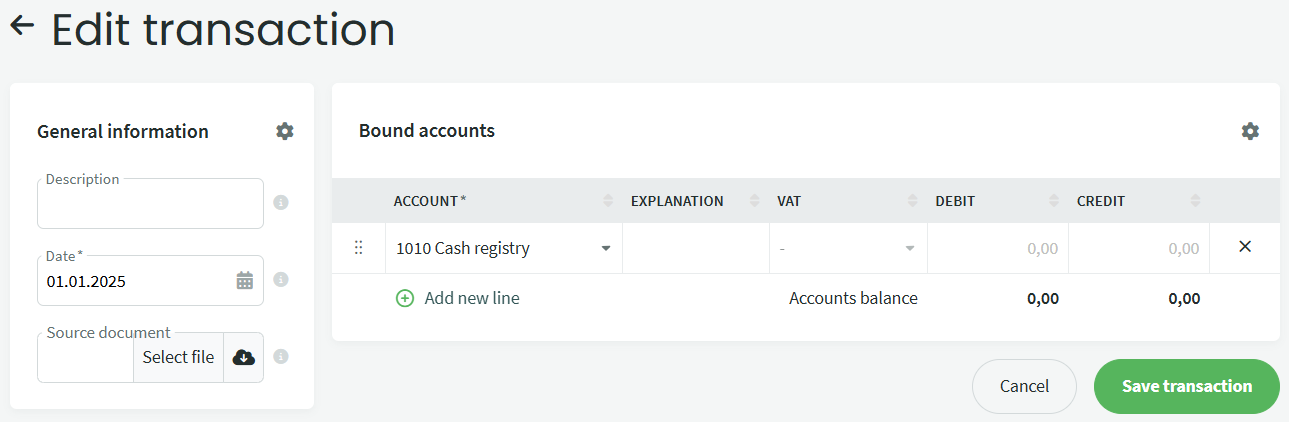

When implementing the SimplBooks accounting software, initial balances must be entered for both new and existing businesses. Until at least one account has an initial balance entered, no entries can be made. If the initial balances are unknown or all are zero for any other reason, at least one account must still have an initial balance entered, with the amount marked as zero.

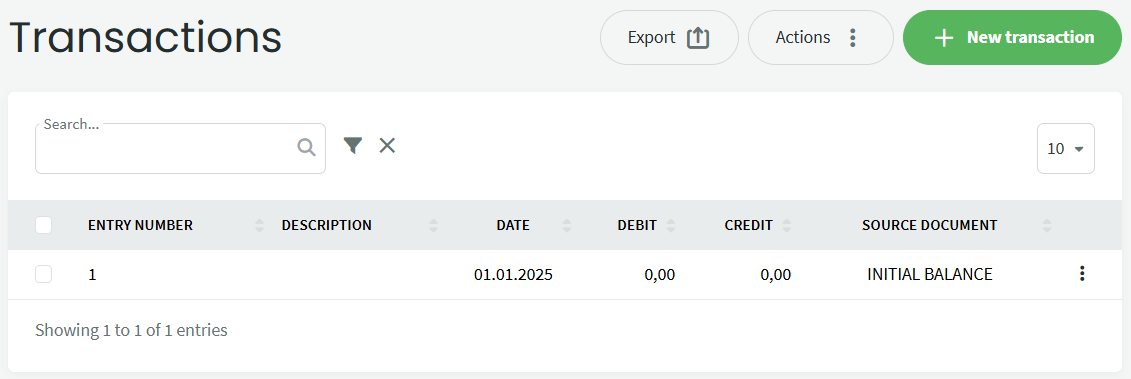

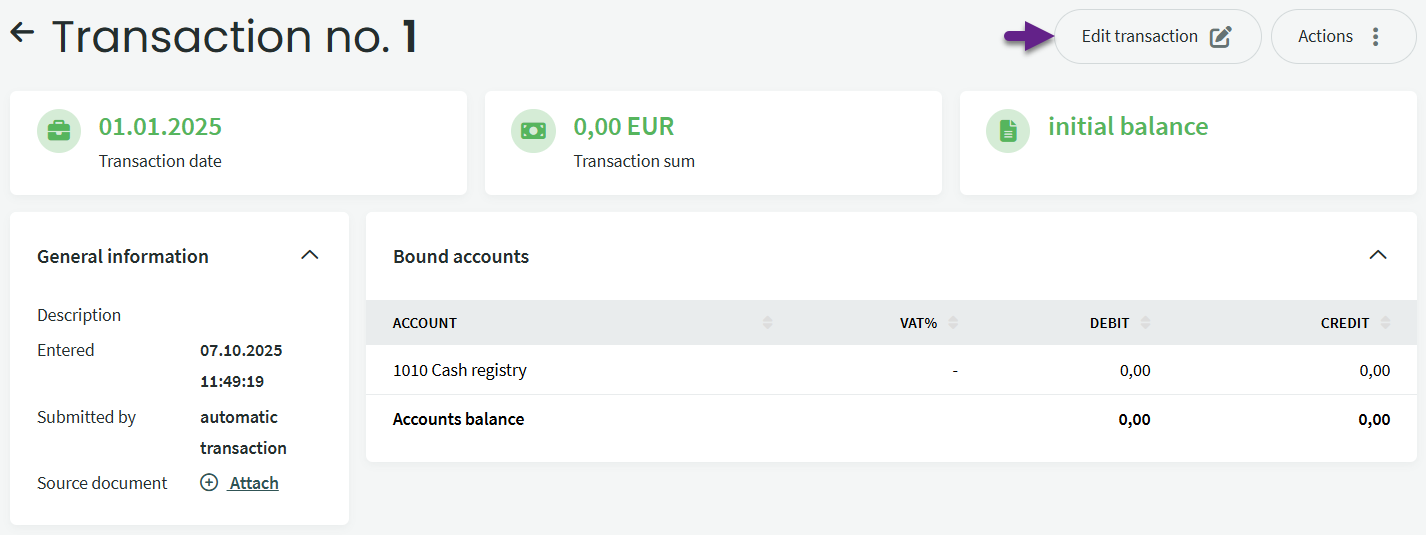

1 When creating a company in the SimplBooks environment, the system automatically adds an initial balance entry. You can find this entry under Accounting -> Transactions, where the “Source document” column will show the information “INITIAL BALANCE”.

Next you should enter the following items included in the initial balances:

1. Transferring claims and liabilities of previous periods to SimplBooks

2. How to bring your existing assets over to SimplBooks?

3. Entering initial warehouse inventory

If you have any additional questions, write to us at support@simplbooks.ee

Leave A Comment?